The Ultimate Guide to Mortgage Refinancing and Approval in Canada

Refinancing a mortgage is like hitting the financial reset button on your home loan. Whether you’re aiming to lower your interest rates, consolidate debt, or tap into home equity, understanding your refinancing options is key to making an informed decision. But with so many banks offering different solutions, how do you choose the right one?

In this comprehensive guide, we’ll break down mortgage refinancing options from CIBC, BMO, and Scotiabank, compare their offerings, and share expert tips from Ratehub on securing mortgage approval. So, grab a coffee, and let’s dive in!

What is Mortgage Refinancing, and Why Should You Care?

Picture this: You signed your mortgage deal a few years ago, but now interest rates have dropped. Or maybe your financial situation has changed, and you need better terms. Refinancing allows you to replace your existing mortgage with a new one, often with better benefits.

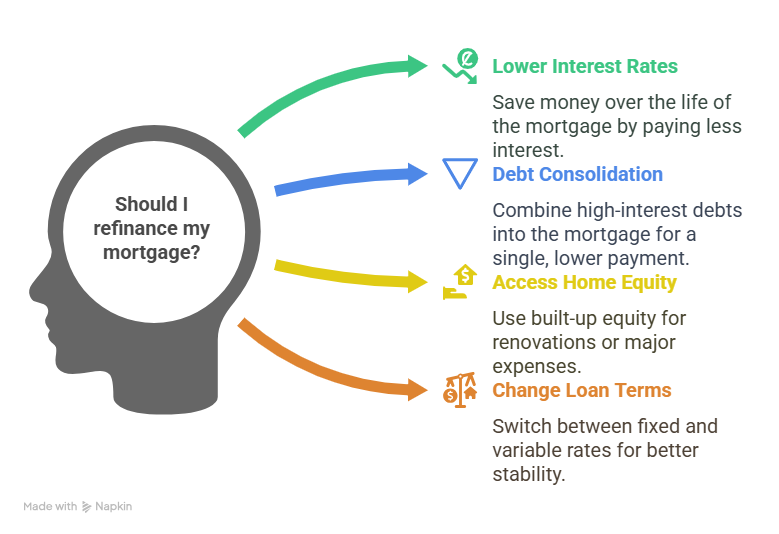

Here’s why homeowners in Canada choose to refinance:

-

Lower Interest Rates – Paying less in interest can save you thousands over the life of your mortgage.

-

Debt Consolidation – Roll high-interest debts (like credit cards) into your mortgage for a single, lower payment.

-

Access Home Equity – Borrow against the equity you’ve built up for renovations, investments, or major expenses.

-

Change Loan Terms – Switch from a variable to a fixed rate, or vice versa, for better stability.

Sounds good, right? Now, let’s see what CIBC, BMO, and Scotiabank bring to the table.

CIBC Mortgage Refinancing: A Solid Choice for Debt Consolidation

Key Benefits of Refinancing with CIBC

-

Competitive Interest Rates – CIBC offers lower rates that can significantly cut down monthly payments.

-

Debt Consolidation – Combine multiple debts into your mortgage for easier management.

-

Home Equity Access – Tap into your home’s value to fund major expenses

Costs to Consider

-

Prepayment Penalties – Breaking your current mortgage early might come with fees.

-

Legal and Appraisal Fees – Additional costs that might add up during the process.

CIBC is a solid choice if you’re looking for a traditional refinancing option with flexible debt consolidation features.

BMO Mortgage Refinancing: Personalized Guidance & Online Tools

What Makes BMO Stand Out?

Unlike some banks that leave you guessing, BMO assigns mortgage specialists to help you navigate refinancing options. Here’s what you get:

-

Personalized Financial Advice – BMO mortgage specialists guide you through refinancing based on your goals.

-

Online Mortgage Tools – Use calculators to compare rates, payments, and affordability.

-

Flexible Prepayment Options – Make extra payments to reduce your loan faster.

Downsides?

-

Interest Rates Might Be Higher – Depending on your credit score and financial situation, you may not get the lowest rates.

-

Approval Process Can Be Lengthy – BMO’s thorough assessment process might take longer than expected.

BMO is best for those who value personalized service and online tools to make informed decisions.

Scotiabank Mortgage Refinancing: The Power of STEP (Scotia Total Equity Plan)

Why Choose Scotiabank?

Scotiabank offers something unique: The Scotia Total Equity Plan (STEP). This allows you to combine different credit products under one plan, making borrowing more flexible.

- Flexible Home Equity Borrowing – As you pay off your mortgage, you gain access to more credit.

- Flexible Interest Rates on Additional Borrowing – Compared to unsecured loans or credit cards.

- Customizable Repayment Options – Choose what works best for your financial situation.

Potential Downsides

-

Complexity – Managing multiple products under STEP might be confusing for some borrowers.

-

Prepayment Fees – Like CIBC and BMO, breaking your mortgage early could cost you.

If you’re someone who wants a flexible, long-term borrowing strategy, Scotiabank’s STEP program is a top contender.

CIBC vs. BMO vs. Scotiabank: Which One Wins?

Interest Rates & Prepayment Options

-

CIBC: Competitive rates with flexible prepayment options.

-

BMO: Higher rates but offers personalized mortgage advice.

-

Scotiabank: Flexible rates on additional borrowing via STEP.

Flexibility & Borrowing Power

-

CIBC: Traditional refinancing structure.

-

BMO: Good for those who need guidance.

-

Scotiabank: Best for ongoing access to home equity.

Best for Customer Support

-

CIBC & BMO: Online tools and customer service.

-

BMO: Dedicated mortgage specialists.

-

Scotiabank: Home financing advisors for complex situations.

If you just want to refinance and save money, CIBC is a great choice. If you need personalized help, BMO is ideal. For long-term financial flexibility, Scotiabank’s STEP plan is hard to beat.

Tips to Get Approved for a Mortgage (According to Ratehub)

Even the best refinancing deal won’t help if you can’t get approved. Here are expert tips to increase your chances

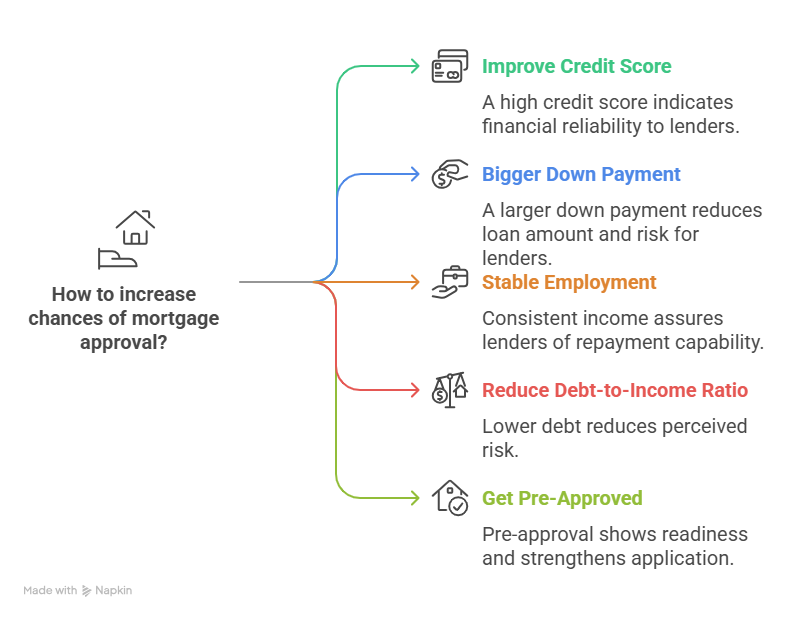

1. Check and Improve Your Credit Score

Lenders love a high credit score! Pay off debts, avoid late payments, and keep credit usage below 30%.

2. Save for a Bigger Down Payment

More money upfront = lower loan amount = better approval odds.

3. Keep Your Job Stable

Lenders prefer applicants with consistent income and employment history.

4. Reduce Your Debt-to-Income Ratio

Less debt means you’re a lower risk. Pay off high-interest credit before applying.

5. Get Pre-Approved

A mortgage pre-approval gives you a clear idea of how much you can borrow and makes you a stronger candidate.

Final Thoughts: Should You Refinance?

Refinancing your mortgage is a powerful financial tool, but only if used correctly. CIBC, BMO, and Scotiabank each offer unique advantages:

-

CIBC is great for lower rates and debt consolidation.

-

BMO is ideal if you need guidance and online tools.

-

Scotiabank shines if you want ongoing home equity access.

Before making a move, weigh your options, consider prepayment penalties, and ensure refinancing aligns with your financial goals.

FAQs

How much does it cost to refinance a mortgage in Canada?

Costs vary but expect legal fees ($500–$1,000), prepayment penalties, and appraisal fees.

2. Is it worth refinancing if interest rates drop by 1%?

Yes! Even a 1% drop can save thousands over your mortgage term.

3. Can I refinance with bad credit?

It’s possible, but you may face higher interest rates or need a co-signer.

4. How long does refinancing take?

On average, 2–4 weeks, depending on the lender and your paperwork.

5. Is mortgage refinancing tax-deductible in Canada?

No, unless you use refinanced funds for investment purposes.