The Ultimate Guide to Venture Capital Trusts (VCTs)

Investing in the stock market can feel like a rollercoaster ride. But what if you could invest in innovative startups while enjoying significant tax benefits? That’s where Venture Capital Trusts (VCTs) come in. If you’ve been wondering whether VCTs are right for you, this guide will break everything down in plain English. So, grab a cup of coffee, and let’s dive in!

1. What is a Venture Capital Trust (VCT)

Imagine you and a group of investors pool your money together to invest in early-stage, high-growth businesses. A VCT is exactly that—a publicly listed investment company that backs promising startups in exchange for equity. In return, investors receive attractive tax incentives from the UK government to encourage them to support these young companies.

A VCT works like a mutual fund but focuses on small, innovative firms that need capital to grow.

2. How Does VCTs Work?

- A VCT operates like a professionally managed fund. Here’s a simple breakdown:

- You invest money into a VCT by purchasing shares.

- The VCT pools that money with other investors’ funds.

- Professional fund managers invest in multiple small businesses, spreading the risk.

- If these businesses succeed, they generate returns for investors in the form of dividends and potential capital appreciation.

The magic of a VCT is its ability to mitigate risk through diversification. Instead of betting on one startup, your money is spread across multiple companies, increasing your chances of success.

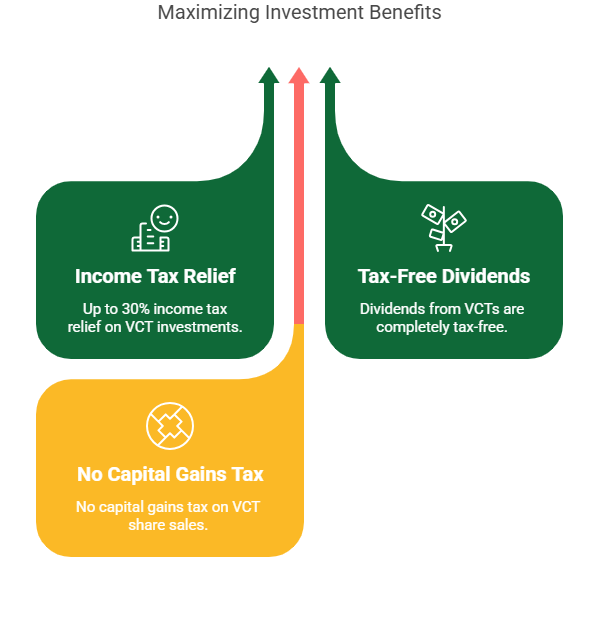

3. The Tax Benefits of Investing in VCTs

One of the biggest draws of VCTs is their tax efficiency. Here’s why savvy investors love them:

✅ Income Tax Relief

Investors can claim up to 30% income tax relief on investments up to £200,000 per tax year.

To qualify, you must hold the shares for at least five years.

✅ Tax-Free Dividends

Any dividends received from a VCT are 100% tax-free, making them a great income-generating investment.

✅ No Capital Gains Tax (CGT)

When you sell your VCT shares, there’s no CGT to pay, provided the company remains within the VCT scheme.

These tax benefits make VCTs particularly attractive to high-net-worth individuals looking to optimize their portfolios.

4. Types of VCTs

Not all VCTs are created equal. Here are the three main types:

1️⃣ Generalist VCTs

Invest in a broad range of companies across multiple sectors.

Ideal for those looking for diversification and long-term growth.

2️⃣ AIM VCTs

Specialize in companies listed on the Alternative Investment Market (AIM).

Higher risk but offer greater liquidity than private startups.

3️⃣ Specialist VCTs

Focus on a specific industry, like biotech or fintech.

Best for investors with expertise in a particular sector.

5. The Risks of Investing in VCTs

VCTs sound amazing, right? But they do come with risks. Here’s what you need to consider:

❌ High-Risk Investment

VCTs invest in startups, which are inherently risky. Many fail, and some never generate profits.

❌ Limited Liquidity

Unlike traditional stocks, VCT shares can be hard to sell due to a smaller market.

❌ Market Fluctuations

Economic downturns impact startups more than established businesses, affecting VCT performance.

Despite these risks, the generous tax benefits can outweigh the downsides for some investors.

6. How to Invest in a VCT

If you’re ready to jump into VCT investing, follow these steps:

Step 1: Research Different VCT Providers

Top VCT providers include Octopus Investments, British Business Bank, and Amati Global Investors.

Step 2: Choose Between New or Existing VCTs

New VCTs raise fresh capital, while existing ones reinvest returns into more companies.

Step 3: Invest via a Broker or Financial Adviser

Some platforms let you invest directly, but a financial adviser can help tailor the best strategy for you.

Step 4: Hold for At Least Five Years

To maximize tax benefits, you need to keep your investment for at least five years.

7. Who Should Invest in VCTs?

VCTs aren’t for everyone. They’re best suited for:

High-income individuals looking to reduce their tax bill.

Experienced investors comfortable with risk.

Long-term investors willing to hold for at least five years.

Those looking for tax-free dividends as an income stream.

If you’re looking for a stable, low-risk investment, VCTs may not be the right choice.

8. Conclusion: Are VCTs Right for You?

VCTs are an exciting opportunity to support innovative startups while enjoying tax perks. But, like any investment, they come with risks. If you’re comfortable with high-risk, high-reward investments, VCTs can be a fantastic addition to your portfolio.

Do your research, consult a financial adviser, and only invest what you can afford to lose. If done right, VCTs can be a powerful tool for wealth growth and tax efficiency.

VCTs are an exciting investment vehicle, but they’re not for everyone. Do your due diligence, and if you’re ready for a high-risk, high-reward journey, they could be just what you’re looking for. Happy investing!

FAQ

Can I invest in multiple VCTs?

Yes! Spreading your investments across different VCTs can reduce risk and improve diversification.

What happens if a VCT company goes bankrupt?

You could lose your investment in that company, but since VCTs invest in multiple firms, losses may be offset by gains elsewhere.

Are VCT dividends paid regularly?

Most VCTs pay annual or semi-annual dividends, but it depends on the performance of their investments.

Can I transfer my VCT shares to someone else?

Yes, but VCT shares are less liquid, and selling them before five years may result in a loss of tax relief.

Do VCTs only invest in UK companies?

Yes, VCTs are designed to support UK-based businesses and must meet HMRC eligibility criteria.